Taxes in Retirement Part 1: Understanding How Your Income is Taxed

Tax Planning Retirement Planning Social Security Financial PlanningBill is 65 years old, and his wife Janet is 63. They are retiring in 2024 with $750,000 in a 401k plan. One of their big concerns: how will their income be taxed? If you are planning for retirement, this is something you need to know.

Watch Now: Taxes in Retirement Part 1: Understanding How Income is Taxed

Watch the Other Episodes in This Series... |

Please Subscribe to our YouTube Channel |

Meet Bill and Janet...

Bill, 65, and Janet, 63, will retire at the end of 2023. They have accumulated $750,000 in their 401(k) accounts. Bill's balance is $425,000 and Janet's is $325,000. They also have a $25,000 cash reserve fund. Bill's Social Security benefit is $1,926. Janet's base benefit is $802 and she will be receiving a spousal benefit. One interesting twist to this case study is Bill's after-tax contributions several years ago. Those total $63,000. Their living expenses total $76,000 per year.

Income Tax Basics...

To understand how Bill and Janet's income will be taxed, we need to understand their income sources. The first place to start is Social Security. Combined we estimate they will receive $32,741 per year from Social Security.

From the cash flow projection, they will need to withdraw $46,862 in the first year to cover their remaining living expenses.

Taxing retirement assets funded with pre-tax contributions:

Most of the withdrawals from their 401(k) accounts are going to be taxed as ordinary income. They will also likely be fully taxed. Roth 401(k) accounts would be treated differently if they had those. Income from a personal or joint account would also be taxed differently.

Taxing Social Security Income

Social Security benefits are at worst partially taxable. To compute how much is taxable, you add half of their Social Security to their other income. If that amount is below $32,000 for a couple, Social Security benefits are not taxed. If that number is between $32,000 and $44,000 half of their benefits are taxable. In this case, half of their Social Security plus their other income is over $44,000. This means 85% of their Social Security benefits are taxable.

What about the after-tax contributions?

Several years ago, Bill contributed $63,000 to his 401k on an after-tax basis. This adds a layer of complexity. Because these contributions were made before the Roth 401k existed, he will need to proceed carefully. Here are his options.

- Roll the after-tax contributions to a Roth IRA - Bill can roll his after-tax contributions to a Roth IRA. Future earnings on that amount will not be taxed if Bill meets the requirements. Keep in mind, only the amount of the after-tax contributions can be rolled to a Roth. Any earnings attributed to those contributions would have to be rolled over to a traditional IRA or he would face a tax liability for them.

- Receive a Check for $63,000 - If Bill rolls his 401(k) balance over to an IRA, he can elect to receive a separate check for $63,000, his after-tax contributions. The rest of the account needs to be rolled over to a traditional IRA. Also, keep in mind, if you want a check for the after-tax money, you have to have a distribution of at least some of the taxable assets.

- Roll all of it to an IRA - Generally speaking, this would not be suggested. Having after-tax money in a traditional IRA creates some record-keeping headaches, If you don't keep track of your basis, you could end up paying taxes twice on that amount

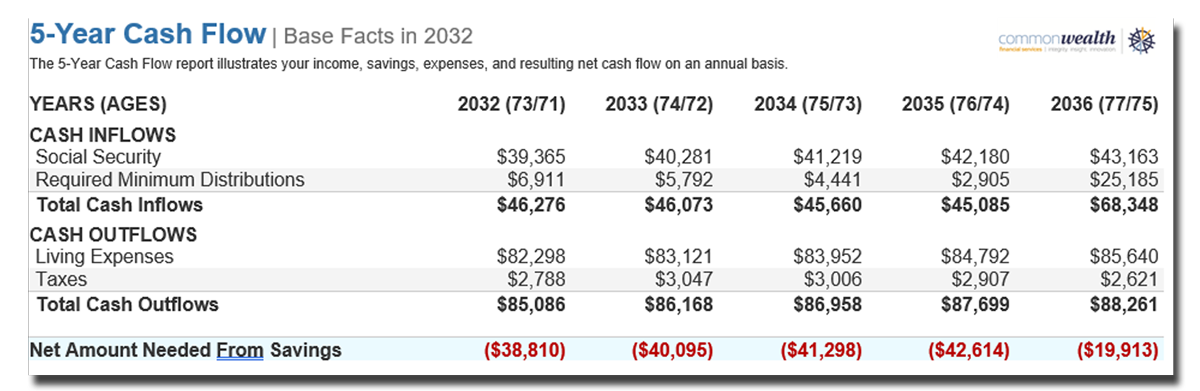

Required Minimum Distributions

One of the most common questions about these types of accounts centers around Required Minimum Distributions, or RMD's. Recent changes in the tax laws have changed the ages for when you must begin these mandatory payments. Bill will reach his required beginning date when he is 73. Janet will be required to start her distributions when she reaches age 75.

This cash flow projection illustrates how the RMD's impact their cash flow situation.

A key thing to consider, as people get older, we often see their spending habits change. They may not be spending as much as they did earlier in their retirement. As a result, they are required to take and report income they may not need to spend. (They can always reinvest the net proceeds of those distributions in other types of accounts). This may result in unwanted tax bills.

Limited planning opportunities for Bill and Janet

Bill and Janet's case is fairly simple and straightforward. This is a common situation we often see with people currently approaching retirement. Unfortunately, there are also few opportunities to do any significant tax planning to reduce their tax bill. For younger investors, building tax diversity into their plans can allow for more flexibility and planning opportunities in retirement.

Bill and Janet will have an interesting planning opportunity, and we will cover that in part 3 of this series.

Do you need help understanding how taxes impact your retirement?

Our team can help you plan for your retirement and a significant part of that process involves understanding how taxes can impact your retirement and your family and how to plan for what you face. If you would like to connect with one of our 8 financial advisors, please complete the form below.

Appearing in this Video

Julie Daley, RICP®

Julie is a financial advisor in St. Clairsville, Ohio.

Evan Brockmeier

Evan is a financial advisor in Marietta, Ohio.

Neal Watson, CFP®

Neal is a financial advisor in Marietta, Ohio.