How Would a 20% Reduction in Social Security Benefits Impact Your Retirement?

Estate Planning Retirement Planning Financial PlanningThere are big problems with the financial side of Social Security. Without legislative action, projections show that in 2033, people receiving Social Security benefits would face a 23% reduction in their annual payments. For most retirees that would be a tough pill to swallow. Today, we illustrate the potential impact it could have on your income and your savings.

Watch Now: How Would a 20% Reduction in Social Security Benefits Impact Your Retirement?

Please Subscribe to our YouTube Channel |

|

Social Security Has Significant Problems

The media has been sounding alarm bells for several years. Social Security is going to have a major financial problem in 2034. At that point, the Social Security trustees project receipts from payroll taxes to be less than what they pay in benefits. If this problem is not resolved, we all face an estimated 23% reduction to our retirement benefits.

Every year, the Social Security trustees release a report on the progress of this doomsday scenario. And of course, financial journalism—whose mantra is "if it bleeds, it leads"—loves to stir people up. A 23% reduction in Social Security benefits would affect more than 90% of us, but just how bad would it be?

In easy numbers, let's say Social Security replaced 50% of your pre-retirement income, a 20% reduction would mean that Social Security now only replaces 40% of your pre-retirement income. This creates a situation where retirees can reduce expenses, take more from their retirement savings, or increase the risk of running out of money during their lifetimes. Those choices don't always sound particularly attractive.

Illustrating The Impact

A couple of weeks ago we met Bill and Janet. In retirement, they depend on Social Security and their 401(k) for their retirement lifestyle. You can read more about the details and assumptions used in their plan, here.

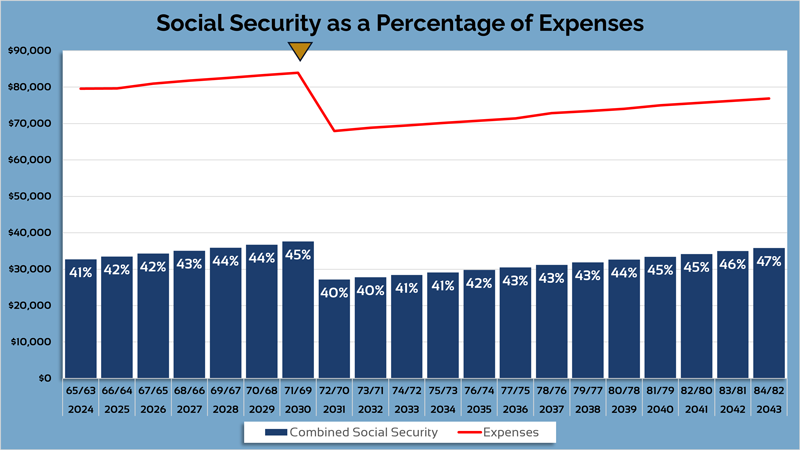

The Baseline Scenario...

In this graph, we see Bill and Janet's expenses represented by the red line. To pay for their needs, they will depend on Social Security (dark blue bars) and withdrawals from their retirement accounts (Yellow bars). At age 75, Required Minimum Distributions will become part of their life (lighter blue bars).

In this scenario, Bill passes away in 2030. You see a decrease in Janet's Social Security as she switches to a survivor benefit. There is also a corresponding decrease in expenses at Bill's Death.

Social Security covers roughly 40-45% of Bill and Janet's expenses during their lifetimes. And remember, Social Security payments are adjusted each year for inflation so this helps them keep pace with the ongoing costs of living.

But we are assuming things are "fixed" or continue to operate just as they always have. We know from the various reports, this is probably not the way things will play out in the future unless the government acts to fix the problems.

How would a 23% reduction impact them?

The light blue bars show Social Security benefits for Bill and Janet. We see the same reduction in benefits at Bill's passing in 2030. But in 2034, we see those benefits drop again. The decrease is 23% or in their case roughly $6,500 per year.

Without a reduction in expenses, Janet will need to withdraw an additional $675 from her retirement accounts to cover the taxes and the funds needed.

In the last year before the cuts to Social Security, Janet was already withdrawing more than 6% from her investments. (This was due to a reduced Social Security benefit after Bill passed away.)

In 2034 when her Social Security income is cut again, her withdrawal rate will exceed 8%, and that adds a lot of risk to the longevity of her savings.

Instead of Social Security covering 40-45% of their expenses, those benefits now only cover a third of the expenses. That is a significant change. To make up the shortfall, Janet will have to rely on larger withdrawals from her retirement savings.

The Impact On Retirement Savings

The potential Social Security income reductions could have a significant impact on your savings. In our example, Janet dies at 82 years old. Should she face a reduction in her Social Security benefits, it could result in nearly $223,734 less in assets transferred to her children.

What this illustration doesn't show is what happens if she lives several years beyond age 82. Without changing her spending habits, this could significantly increase her risk of running out of money before she dies—something known as longevity risk.

It doesn't consider other potential problems she could face. A major bear market or a nursing home stay could amplify the impact of something like this even more.

Failing to fix this problem is something that can impact all of us.

Does Social Security Get Fixed?

None of us really know the answer to this question. But it is probably likely that something will be done to improve the ability of the program to pay its benefits. It could mean higher taxes, increasing the retirement age, or a combination of multiple things. It will be a hotly debated and polarizing topic in the years to come. But we should be aware that a failure to correct the problems will have an impact on your income and your savings. One of the biggest things you can do as you plan for your retirement is to be flexible. There are any number of things that can cause problems for the financial side of your retirement and it may force you to adjust how you do things.

Keep in mind, we can help you illustrate the potential impact on you and offer some suggestions about how to make changes to reduce the possible impact. If you would like to know more, fill out the form below and one of our advisors will reach out to you.

Appearing in This Video

Nikki Lude, CFP®

Nikki is a financial advisor in Woodsfield, Ohio.

Vince McManus

Vince is a financial advisor in Parkersburg, West Virginia

Neal Watson, CFP®

Neal is a financial advisor in Marietta, Ohio.